Case: M-PESA

Section 6 (3 pm), Group 3

MI021 Computers in Management

Group Members:

Chandler Moore

Ryan Gavin

Vince Murphy

Angel Chen

Galassia Grassetto

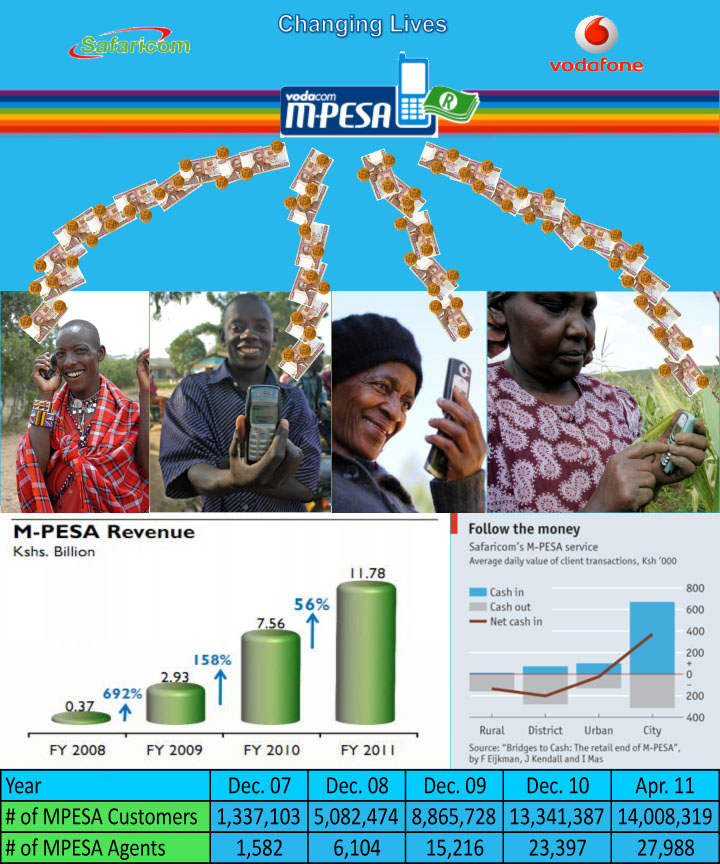

M-PESA is a mobile phone based money transfer service for Safaricom, which is a Vodafone affiliate, which launched in Kenya in 2007. The company allows users to save money, to send balances via mobile phone to other users such as sellers of goods and services, and to redeem deposits for regular money. M-PESA is facilitated by a network of retail agents and has gained widespread trust and financial inclusion into Kenya’s economy since its launch. People discovered it was more efficient than going to the post office, transporting money in cash, or using bus companies.1 Popularity also increased due the minimal involvement of banks. M-PESA has been increasingly incorporated into the culture. As of March 2011 there were 13.8 million recorded users.2 In May of 2011 it reported revenue growth of 56 percent, from 7.56 billion kshs (USD 75 million) to 11.78 kshs (USD 112 million). 2 They are now seeking to expand into other countries and will face new barriers to entrance while maintaining their market presence.

M-PESA is in the mobile money services industry, providing financial services with branchless banks. The mobile money industry opened as many mobile businesses indicated their interests – the development of M-PESA, Orange’s decision to deploy mobile money in the Ivory Coast etc.3 The mobile industry in Kenya is now in the origination phase4, since awareness is prevalent and firms need to improve conditions by investing to lower regulatory barriers and share information and hence improve speed.

The basic tool that is used to employ M-Pesa’s technology is the mobile phone. The mobile phone is unique because it is transcending social classes. Sara Corbett of The New York Times Magazine writes that “Unlike fixed-line phone networks, which are expensive to build and maintain and require customers to have both a permanent address and the ability to pay a monthly bill, or personal computers, which are not just costly but demand literacy as well, the cellphone is more egalitarian, at least to a point.”5 In addition to this, for every additional 10 mobile phones per 100 people in a developing country, GDP rose 0.6% to 1.2%. 6

The makers of M-Pesa were able to capitalize on the vast capabilities of the mobile phone. The two well-known companies that created M-Pesa are Vodafone and Safaricom. However, the company behind the software of M-Pesa was one based in Cambridge, called Sagentia. Although they played a small role, it was an extremely important one. The firm not only wrote the software for M-PESA, they also designed the business processes, and provided operational and technical support during the pilot and after launch.7 There were many iterations of the current platform and it started out as only peer-to-peer file transfer service. 7 The team then did further research, such as by following usage patterns and turned M-Pesa into what it is now, which even allows users to pay bils.7 M-Pesa uses different technologies in Kenya and Tanzania. In Kenya, they use something called an SIM Tool Kit (STK) and in Tanzania they use USSD. Both work on almost every phone on the market and run on the GSM standard. With the STK case, an application is set-up on a SIM card, allowing for a simpler user-interface. Using USSD, a short number has to be entered and then the menu has to be sent back, which can be a bit time consuming.11 In order to get the service running, a customer sets up an account with Safaricom and sets up their account using the technologies above. Next, the person visits an M-Pesa agent and loads up their e-Wallet. They can then transfer this money via SMS text message.4

M-Pesa has been able to create significant advantages that make it hard for rivals to compete. First off, M-Pesa dominates the current market in Kenya, where it was first launched. In fact, as of Nov. 2009, about 25% of Kenya’s population were M-Pesa subscribers, that’s 8.6 million people and the number is only growing.8 In addition to having a large market share, the company also boasts robust customer satisfaction numbers. A recent survey found that 98% of customers are happy with their M-Pesa service and 84% claim that if they lost the service, it would have a significant negative effect on their lives.9 M-Pesa has become so successful because it was launched in the right place at the right time. There have been numerous competitors, and although M-Pesa has struggled a bit in other areas of the world, including Tanzania, it is the dominant player in Kenya. Two problems that M-Pesa faced when starting out were that they had to gain the trust of the people that they were going to be serving and they had to overcome the hurdle of network effects. Although these were difficult problems, M-Pesa is now able to wield them as powerful weapons. They were able to achieve branding, which is essentially trust, through their parent company, Safaricom. They did this by providing a simple marketing message: “send money home.”10 As a matter of fact, some market research has now shown that M-Pesa is even a stronger brand than Safaricom.10 From this successful branding, more and more people started jumping on the M-Pesa train, allowing them to leverage network effects on their rivals. This is because most of their money transfers are from person-to-person, so the more users of M-Pesa there are, the more likely that new customers are going to join. This also creates a sort of switching cost for customers because in order to switch, they would be leaving behind all the customers that currently use M-Pesa’s service.

Safaricom has first-mover advantage over its competitors because its product, M-PESA, was the first mobile-phone money transfer service in Kenya. Safaricom’s first-mover advantage has allowed them to capture the mobile-phone money transfer market and to continue to gain leverage over its competitors. M-PESA has been so dominant due to the concept of network effects. It continues to be more valuable as more people use the M-PESA mobile phones. According to Mohit Agrawal, a telecommunications expert, Safaricom has been able to leverage itself and rapidly expand its customer base by “keeping the pricing of the M-PESA product very transparent and lower than other alternatives. Free registration and no monthly fee helped the agents in persuading the potential user to subscribe to the service.”12

In early 2009, Zain Group, a telecommunications company similar to Safaricom, released a mobile commerce service called “Zap” in Kenya, Tanzania, and Uganda to compete with M-PESA. Like M-PESA, Zain customers can register for the Zap banking and payment services for free.13 Since Safaricom launched M-PESA in Kenya in March of 2007, nearly two years before Zain launched Zap, Safaricom has had a significant market advantage. The M-PESA brand continued to be more valuable as more people began to use these mobile phones and because of the absence of other competitors for a span of two years. By 2011, Safaricom’s market has expanded to Tanzania, Afghanistan, and South Africa.

One way Zain is trying to compete with Safaricom is by expanding its market even farther. As of June 30, 2011, Zain has a commercial presence in Sudan, Saudi Arabia, Jordan Lebanon, Iraq, Kuwait, and Bahrain.14 Also, Zain may be able to take advantage of M-PESA’s “cash float” problems. M-PESA relies on banks for its liquidity. In Bukura, Kenya, a majority of the transactions tend to be withdrawals. M-PESA agents must process these withdrawals by maintaining their cash float by traveling to the bank on a regular basis. Since most of the banks are located in urban centers, these trips tend to be very time consuming and can cost M-PESA agents a portion of their income. This is not very efficient as some customers must travel to these urban areas to obtain their money.15

The biggest challenge that M-PESA faces is due to cash float constraints. M-PESA retail outlets cannot always meet requests for withdrawals, especially large withdrawals.16 Also, the agent commission structure discourages outlets from handling these large withdrawals.16 If they take too many withdrawals, especially large withdrawals, then they may run out of cash to facilitate other deposits later on. This forces customers to split their transactions up over time, which is often inconvenient. It also discourages customer trust in M-PESA as a mechanism for long-term saving. The challenge that still remains for M-PESA is to become a “vehicle for delivery of a broader range of financial services to the bulk of the Kenyan population.” 16 Currently, there is limited evidence that people are willing to use the M-PESA account itself as a store of value. However, if the company gains more trust this evidence may increase. M-PESA would also need to connect to a broader range of financial institutions. In order to do this the Central Bank of Kenya would need to finalize regulations to allow non-bank outlets and platforms such as M-PESA as a channel for formal deposit-taking.16

Tools from the developed world are being transformed for use in the developing world. M-PESA took advantage of the falling costs of mobile phone technology enabling them to adapt the technology to support financial services so that mobile banking has caught on within poor countries. The low cost and the need for financial services in developing nations means that M-PESA has the potential to reach even more people of all socio-economic levels. This potential is being realized in Kenya. They have reached nearly 40 percent of the adult population in about 2 years of operation. 17 Their network of M-PESA agents is only getting larger. In Kenya, M-PESA clearly dominates in money-transfer largely due to their early entry. In the future, M-PESA may have issues breaking into or maintaining success in other markets as there success in Kenya was based greatly on strong latent demand for domestic remittances, poor quality of available financial services, a banking regulator that permitted Safaricom’s experimentation, and a mobile communications market already dominated by Safaricom.17 Although their success was aided by these conditions they also succeeded in part due to their design of the product. They made it the product easy to use in order to overcome the adoption barrier. Safaricom successfully implemented a product that overcame adverse network effects and gained people’s trust ensuring growth of the company. M-PESA in Kenya will most likely expand, but we will have to wait and see if they can break into new markets profitably in other countries or if they establish M-PESA as a channel for formal deposit taking.

Endnotes

_________________________________

1 Policy brief on financial inclusion in India: The M-PESA model – an overview. (2011, June). Retrieved from www.slideshare.net/indicusanalytics/policy-brief-on-financial-inclusion-in-india-the-mpesa-model-an-overview

3 Mobile money for the unbanked. (2009). Retrieved from http://mmublog.org/wp-content-files_mf/annualreport2009.pdf

4 Mobile money for the unbanked. (2011). Retrieved from http://mmublog.org/wp-content/files_mf/mmu_report98.pdf

5 Corbett, S. (2008, April 18). Can the Cellphone Help End Global Poverty? Retrieved from New York Times Magazine website: http://www.nytimes.com/2008/04/13/magazine/13anthropology-t.html?pagewanted=all

6Perry, A., & Wadhams, N. (2011, January 31). Kenya’s Banking Revolution. Retrieved from TIME Magazine website: http://www.time.com/time/magazine/article/0,9171,2043329,00.html

7 Morawczynski, O. (2009, July 14). What You Don’t Know About M-Pesa. Retrieved October 11, 2011, from http://technology.cgap.org/2009/07/14/what-you-dont-know-about-m-pesa/

8 Agrawal, M. (2010, January 19). M-Pesa: Transforming Millions of Lives. Retrieved October 11, 2011, from http://www.telecomcircle.com/2010/01/m-pesa/

9Mas, I., & Radcliffe, D. (2010, March). Mobile Payments Go Viral: M-Pesa in Kenya. Retrieved from Bill and Melibda Gates Foundation website: http://siteresources.worldbank.org

10Mas, I., & Ng’weno, A. (2009, December). . Three Keys to M-PESA’s Success: Branding, Channel Management and Pricing. Retrieved from Bill and Melinda Gates Foundation website: http://mmublog.org

11 Camner, G., Pulver, C., & Sjoblom, E. (n.d.). What Makes a Successful Mobile Money Implementation? Learnings from M-PESA in Kenya and Tanzania. Retrieved from http://mmublog.org

12 Agrawal, M. (2010, January 19). M-Pesa: Transforming Millions of Lives. Retrieved from Telecom Circle website: http://www.telecomcircle.com/2010/01/m-pesa/

13 Zain dials up mobile banking in Africa with Zap. (n.d.). Retrieved from Zain website: http://www.zain.com/muse/obj/lang.default/portal.view/content/Media%20centre/Press%20releases/ZapLaunchAfrica

14 Our Presence. (n.d.). Retrieved from Zain website: http://www.zain.com/muse/obj/lang.default/portal.view/content/About%20us/Worldwide%20Presence

15 Pickens, M., & Morawczynski, O. (2009, August). Poor People Using Mobile Financial Services: Observations on Customer Usage and Impact from M-PESA. Retrieved from http://www.cgap.org/p/site/c/template.rc/1.9.36723/

16 Mas, I., & Radcliffe, D. (2010). Mobile payments go viral: M-PESA in Kenya. Retrieved from http://pymnts.com/mobile-payments-go-viral-m-pesa-in-kenya/

17 Jack, W., & Suri, T. (2010). The economics of M-PESA. Retrieved from http://www.mit.edu/~tavneet/M-PESA.pdf

No comments:

Post a Comment